From the Abraham Accords to AI to FTAs: how to trade the new Middle East

Renée Friedman, PhD

Global Head of Research

EXANTE

From the Abraham Accords to AI to FTAs: how to trade the new Middle East

The global economic and geopolitical landscape is shifting under the combined weight of uneven monetary policy normalisation, ongoing tariffs and tariff effects, an unprecedented adoption of new technologies, and a new phase of strategic realignment in the Middle East.

For investors and policymakers across the GCC, the task is to understand how these forces interact. Those who map the connections early will be best positioned to capture new avenues for trade, diversify exposure, and manage the next cycle of regional and global risk.

Renée Friedman, PhD

Global Head of Research

EXANTE

Global macro economic developments 2025

Monetary Policy: Divergence and Challenges

Sticky inflation, tariff risks and rising debt loads limit how far and how fast central banks can cut

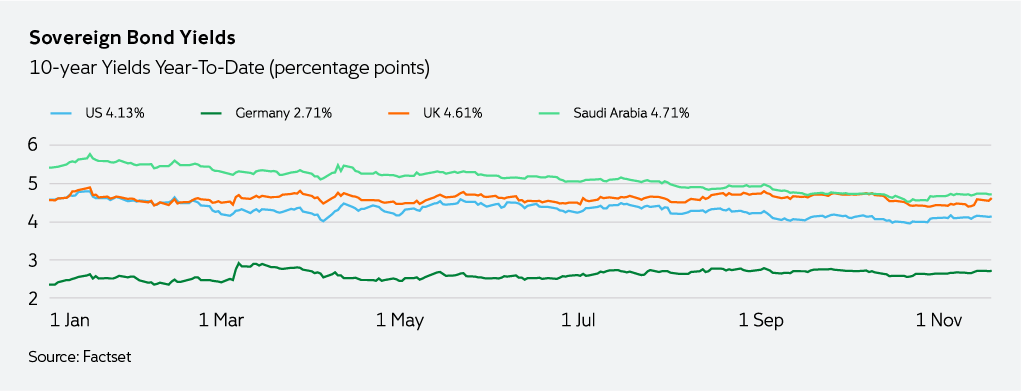

Across major economies, and with the notable exception of Japan, global monetary policies largely continued to loosen throughout 2025. The Federal Reserve held rates steady for much of the year, resuming cuts only in September and October in 25 bps increments. The European Central Bank and other G7 central banks have taken similarly cautious paths, easing in response to cooling inflation and softening growth. This overarching challenge is familiar. A delicate balancing act between supporting labour markets while still anchoring inflation expectations.

Bond market performance has been largely positive due to this normalisation. But inflation remains stickier than expected across many economies and US tariff uncertainty imposes additional upward pressure for 2026. At the same time, there are concerns over growing debt levels. Six of the G7 countries are expected to see debt-to-GDP exceed 100 percent in 2025, sharpening concerns around fiscal flexibility.

This dynamic is particularly acute in the US and UK, where higher borrowing costs and narrowing fiscal headroom are negatively impacting market sentiment. As questions around debt sustainability rise and sovereign debt continues to flood the market, investors may demand higher yields, tightening financial conditions and adding pressure to public finances. The interaction matters. Higher debt levels and rising debt loads can amplify market volatility, especially if the cost of capital increases. In that event, companies may struggle to fulfill their capex goals on AI, thereby potentially busting the bubble that has driven equity markets throughout this year.

The growth of fiscal dominance

Elevated debt heightens political pressure on central banks and complicates the path of monetary policy

Rising debt burdens have brought the spectre of fiscal dominance back into focus. In such an environment, central banks face growing political pressure to keep rates low or to accommodate government spending through money creation. It can reignite inflation, undermine central bank independence, and erode confidence in state institutions.

In the United States, these concerns have sharpened. Investor unease stepped up several notches following President Trump’s attempts earlier this year to dismiss Federal Reserve Governor Lisa Cook and his public criticism of Chair Jerome Powell for not cutting rates more quickly. Attention is increasingly being focussed on the President’s choice for Powell’s successor, with his term as Chair set to end in May 2026. With inflation now near 3 percent in the US, if President Trump continues to push for lower headline rates, it could push real interest rates into negative territory. This, in turn, would encourage borrowing and investment and certainly risk higher inflation.

The tension between political expediency and monetary prudence is likely to intensify as debt levels remain elevated and the 2026 US midterms approach. These dynamics, however, should have limited impact on the GCC. According to the International Monetary Fund (IMF), GCC economies are expected to sustain solid growth with low inflation and strong current account and external financial positions over the next five years. The region’s substantial sovereign wealth funds provide an additional buffer against fiscal stress, though the World Bank notes that downward pressure on oil prices will weigh on government revenues, increasing fiscal strains in Kuwait, Oman and the UAE.

AI lifts markets, but risks accumulate

Enthusiasm for all things AI lifted global equities to new highs, but the rally is vulnerable

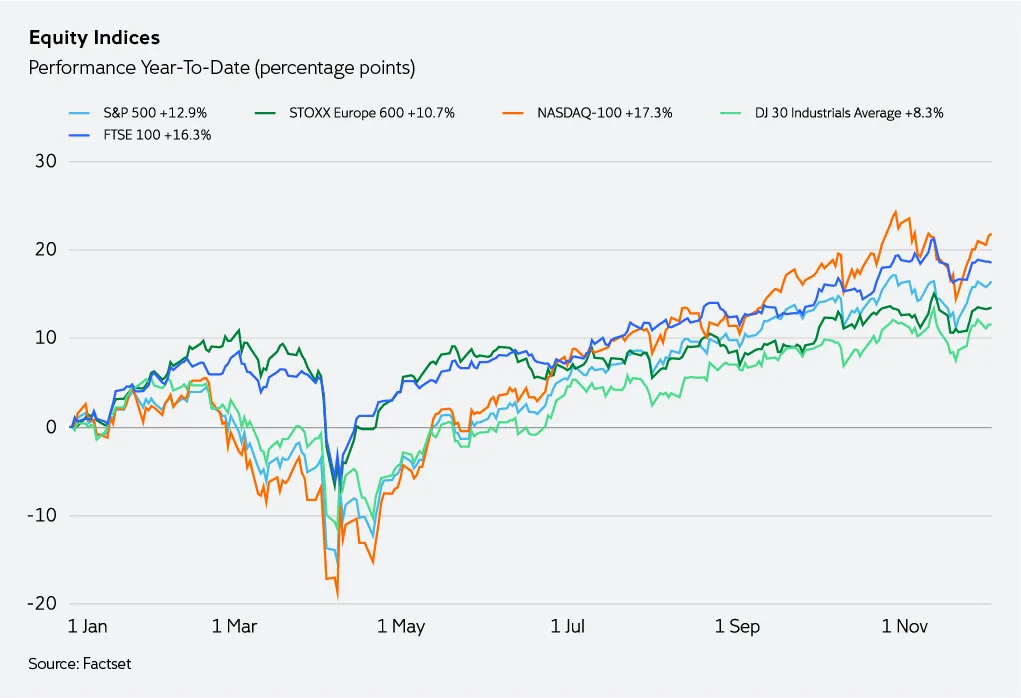

Global equity markets have recovered steadily since the April “Liberation Day” sell-off. Expectations of Fed policy easing and continued momentum in the AI revolution have pushed indices to fresh highs. Yet the headline rally masks a more nuanced backdrop. Markets are late in the cycle and the bull market euphoria remains tightly linked to the Fed’s next moves. Without further rate cuts, the current momentum could prove fragile.

At the same time, additional easing — especially if paired with expanded fiscal stimulus — may accelerate the cycle rather than extend it. As Andrew Slimmon at MorganStanley notes, the more liquidity, the higher the speculative stocks rise. And the faster the bubble inflates, the faster the market moves through the “euphoria stage”, increasing the risk of a sharper reversal.

AI lifts markets, but risks accumulate

Enthusiasm for all things AI lifted global equities to new highs, but the rally is vulnerable

Global equity markets have recovered steadily since the April “Liberation Day” sell-off. Expectations of Fed policy easing and continued momentum in the AI revolution have pushed indices to fresh highs. Yet the headline rally masks a more nuanced backdrop. Markets are late in the cycle and the bull market euphoria remains tightly linked to the Fed’s next moves. Without further rate cuts, the current momentum could prove fragile.

At the same time, additional easing — especially if paired with expanded fiscal stimulus — may accelerate the cycle rather than extend it. As Andrew Slimmon at MorganStanley notes, the more liquidity, the higher the speculative stocks rise. And the faster the bubble inflates, the faster the market moves through the “euphoria stage”, increasing the risk of a sharper reversal.

Volatile trade policy, resilient Gulf

US tariff shifts add uncertainty, but the GCC stays resilient and continues to broaden its FTA ties

Trade and tariff policies have been highly volatile in 2025 following President Trump’s decision on 2 April to impose a slew of country-specific tariffs under the International Emergency Economic Powers Act (IEEPA). Their legality is now before the US Supreme Court. Even if the Court rules against them, it does not mean they will be removed. The administration is likely to quickly re-impose similar measures using other provisions, most notably Section 122 of the 1974 Trade Act, which allows a temporary blanket tariff of up to 15% for a maximum of 150 days, and then negotiate from there.

To date, the GCC has been relatively insulated from the most disruptive effects of Trump’s tariffs. Although uncertainty in global supply chains persists, the Gulf states’ strategic positioning as energy suppliers and logistics hubs has provided a buffer against these headwinds. Instead the region has continued to seek out new free trade agreements (FTAs). The block collectively holds 12 agreements. Individual members, most notably the UAE, have concluded more than 25 bilateral comprehensive economic-partnership agreements (CEPAs) with countries, including Australia, India, Indonesia, Russia, South Korea, and Turkey.

At the same time, the GCC’s long-running push for economic diversification and its position as a connector between East and West seem increasingly prescient. The region’s neutrality and economic pragmatism have made it an attractive partner. Nevertheless, as Sahan Alhasan, Senior Fellow for Middle East policy at Institute for International Strategic Studies (IISS) notes, the GCC remains vulnerable to swings in oil prices. This impacts its ability to fund diversification programmes. Intra-GCC trade frictions, stalled FTA negotiations with China, the European Union, India and Japan, and a worsening regional security environment also pose meaningful challenges to the bloc’s geo-economic ambitions.

Currency Dynamics: The Dollar and De-Dollarisation Debate

Currency narratives evolve, but the GCC’s dollar pegs look stable for now

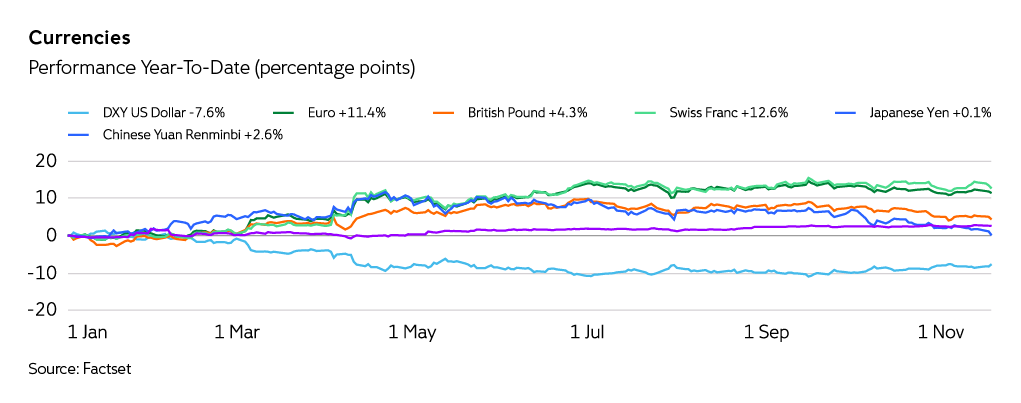

Currency markets in 2025 have been characterised by dollar volatility, with the dollar down over 7 percent year-to-date. This decline reflects a broad sell-off of US assets after the announcement of “Liberation Day” tariffs and on rising concerns around US debt and fiscal sustainability. These developments have brought fresh attention to de-dollarisation efforts, particularly within the BRICS nations (Brazil, Russia, India, China, and South Africa). Although the dollar remains the world’s dominant reserve currency, its share of global reserves has continued the gradual decline that began over a decade ago. While no alternative currency is positioned to replace it in global trade or finance, diversification by central banks and trading blocs is likely to continue.

For the GCC, with most currencies pegged to the dollar, these dynamics present a complex set of considerations. The dollar peg has long provided stability and supported trade integration, but it also means that regional monetary conditions are effectively imported from the Federal Reserve. As global economic power continues to tilt eastward and new payment systems develop, GCC policymakers are likely to reassess the long-term implications of their currency frameworks. However, no immediate changes appear imminent.

Commodities: New Dynamics in Energy and Beyond

Softer oil prices and shifting supply patterns reinforce the GCC’s push to diversify beyond hydrocarbons

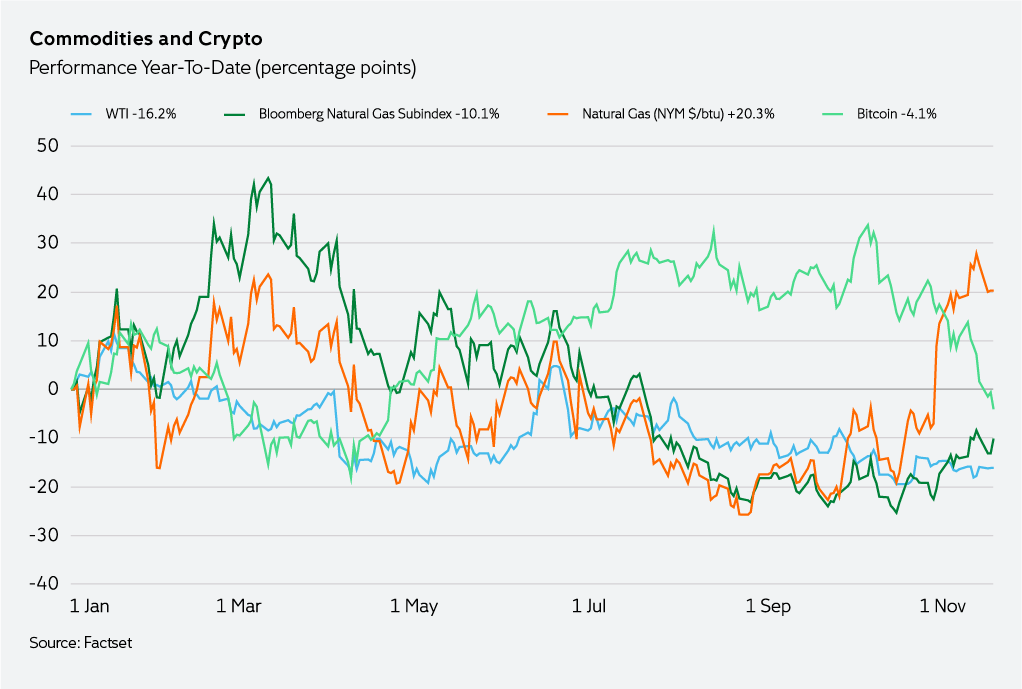

The commodities landscape evolved significantly in 2025, with implications well beyond traditional price cycles. For the GCC, the energy transition continues to reshape the long-term outlook for oil and gas, even as near-term demand remains relatively robust.

Sanctions on Russia, Iran, Venezuela, India, and China have altered pricing dynamics and redirected trade flows, often positioning the GCC as a stabilising supplier. Yet, oil prices are expected to continue to fall, particularly as OPEC+ has boosted production more rapidly than many oil market observers had expected. According to PwC, by September OPEC+ had restored the 2.2m barrels per day (b/d) in production that eight members – including Saudi Arabia, Iraq, the UAE, Kuwait and Oman – had ‘voluntarily’ withdrawn from the market in January 2024. Other members, such as Bahrain, continue to operate under the group-wide quotas set in October 2022.

Additional production growth by non-OPEC+ producers, alongside concerns about softer demand, contributes to the downward pressure. This strengthens the strategic imperative for diversification. Oil still represents 28.8 percent of GCC GDP (2024) and accounts for up to 64 percent of government revenues (2023).

At the same time, the region is investing heavily in renewable energy, green hydrogen, and critical minerals linked to energy transition. This reflects a strategic recognition that commodity dominance requires evolution. Saudi Arabia, for instance, signed a critical-minerals agreement in May 2025 that would help the US ensure a secure and uninterrupted supply of uranium, metals, permanent magnets, and rare earth elements. This transition to renewable energy production may prove critical. Global decarbonisation efforts, rising energy security concerns and the growing need for affordable power for AI data centres are all reinforcing momentum behind renewable energy investment.

Global Geopolitical Developments: Paradigm Shifts

The Abraham Accords and their economic dividend

New diplomatic alignments are translating into deeper economic integration and cross-border collaboration.

The Middle East continues to transform in ways that, just seven years ago, would have seemed impossible. The Abraham Accords, signed in September 2020 between Israel, the UAE, and Bahrain, created a diplomatic normalisation framework that fundamentally altered regional dynamics and paved the way for substantial economic cooperation. Morocco and Kazakhstan have since joined the accords. Sudan signed an Abraham Accords Declaration in January 2021, but did not conclude a bilateral agreement with Israel following the government’s overthrow in October 2021, its descent into civil war in April 2023, and its subsequent realignment toward Iran.

The tangible economic fruits of these agreements have begun to materialise. The Israel – UAE Comprehensive Economic Partnership Agreement (CEPA), signed in May 2022 and implemented in March 2023, represents the first major trade deal emerging from the Abraham Accords. It has supported rising bilateral trade, expanding technology partnerships, and deeper investment flows.

According to the UK Parliament’s International Affairs and Defence Section, the UAE is now Israel’s second- largest trading partner in the region, after Turkey. Despite political pressures from neighbouring Arab states and from within the UAE itself, as noted by Giorgio Cafiero at the Middle East Council on Global Affairs, bilateral trade has remained largely insulated, reflecting a willingness to shrug off public opinion in favour of shared economic interests and long-term strategic alignment.

In 2024, UAE – Israel bilateral trade reached $3.2 billion, a 1 percent increase over the previous year. A similar agreement between Israel and Bahrain has yet to be concluded, though talks began in 2022, and Israel’s trade arrangements with Morocco remain more limited. In November 2025, Saudi Crown Prince Mohammed bin Salman (MBS) visited the White House to meet with US President Donald Trump, discussing terms for Saudi Arabia potentially joining the Accords.

Cooperation across technology, agriculture, tourism and financial services is likely to deepen. The Atlantic Council observes that shifting geopolitical dynamics and technological change have underscored the value of stronger cooperation between Israel and its neighbors — along with the importance of overcoming long-standing rifts that impede the region’s economic growth potential. The normalisation process has created genuine economic value and new channels for innovation and growth. For the UAE in particular, these partnerships have reinforced its position as a regional hub connecting diverse markets and fostering collaboration that can transcend historical regional divisions.

Global Geopolitical Developments: Paradigm Shifts

The Abraham Accords and their economic dividend

New diplomatic alignments are translating into deeper economic integration and cross-border collaboration.

The Middle East continues to transform in ways that, just seven years ago, would have seemed impossible. The Abraham Accords, signed in September 2020 between Israel, the UAE, and Bahrain, created a diplomatic normalisation framework that fundamentally altered regional dynamics and paved the way for substantial economic cooperation. Morocco and Kazakhstan have since joined the accords. Sudan signed an Abraham Accords Declaration in January 2021, but did not conclude a bilateral agreement with Israel following the government’s overthrow in October 2021, its descent into civil war in April 2023, and its subsequent realignment toward Iran.

The tangible economic fruits of these agreements have begun to materialise. The Israel – UAE Comprehensive Economic Partnership Agreement (CEPA), signed in May 2022 and implemented in March 2023, represents the first major trade deal emerging from the Abraham Accords. It has supported rising bilateral trade, expanding technology partnerships, and deeper investment flows.

According to the UK Parliament’s International Affairs and Defence Section, the UAE is now Israel’s second- largest trading partner in the region, after Turkey. Despite political pressures from neighbouring Arab states and from within the UAE itself, as noted by Giorgio Cafiero at the Middle East Council on Global Affairs, bilateral trade has remained largely insulated, reflecting a willingness to shrug off public opinion in favour of shared economic interests and long-term strategic alignment.

In 2024, UAE – Israel bilateral trade reached $3.2 billion, a 1 percent increase over the previous year. A similar agreement between Israel and Bahrain has yet to be concluded, though talks began in 2022, and Israel’s trade arrangements with Morocco remain more limited. In November 2025, Saudi Crown Prince Mohammed bin Salman (MBS) visited the White House to meet with US President Donald Trump, discussing terms for Saudi Arabia potentially joining the Accords.

Cooperation across technology, agriculture, tourism and financial services is likely to deepen. The Atlantic Council observes that shifting geopolitical dynamics and technological change have underscored the value of stronger cooperation between Israel and its neighbors — along with the importance of overcoming long-standing rifts that impede the region’s economic growth potential. The normalisation process has created genuine economic value and new channels for innovation and growth. For the UAE in particular, these partnerships have reinforced its position as a regional hub connecting diverse markets and fostering collaboration that can transcend historical regional divisions.

Regional Realignments: Turkey, Syria, and Evolving Relationships

Shifting ties highlight the Gulf’s increasingly multi-aligned strategy

The geopolitical architecture of the Middle East has continued to shift in unexpected directions. President Trump’s meeting with UAE leadership in May 2025, followed by his meeting with Syria’s new president on 10 November and subsequent meetings with Saudi Arabia’s Crown Prince Mohammed bin Salman, signals a complex recalibration of regional relationships.

Turkey’s evolving posture toward Syria and the broader region, acting as both a bridge and a counterbalance to Iran, is shaping this new environment. At the same time, shifting dynamics in US – European – GCC relations has added further fluidity. The GCC has thus far managed to maintain constructive relationships across multiple and sometimes competing power centres while pursuing its own strategic and economic interests. This is reflected in the reported agreement, highlighted by Bloomberg news, between President Trump and Crown Prince Mohammed bin Salman to authorise the sale of advanced artificial intelligence chips to the Saudi firm Humain as part of a broader US-Saudi AI agreement.

These developments fit within a broader pattern of expanding GCC strategic autonomy. Rather than aligning exclusively with any single major power, Gulf states are pursuing multi-aligned foreign policies designed to preserve flexibility and maximise economic opportunity. This pragmatic approach recognises that the multipolar world of 2025 requires different strategies than the bipolar or unipolar systems of the past.

Regional Power Dynamics and Strategic Partnerships

Shifting alliances are driving a more economically aligned regional order

Power structures in the Middle East are evolving as GCC states move from being viewed primarily as a collection of energy-rich states to being recognised as increasingly sophisticated economies with clear and ambitious longterm development agendas. Saudi Arabia’s Vision 2030, the UAE’s economic diversification agenda and similar initiatives across the region are reshaping domestic economic models and external relationships.

Regional alliances are increasingly driven less by ideology or security alignment and more by shared economic interests and development priorities. The China-brokered rapprochement between Iran and Saudi Arabia represents a significant shift that has reduced regional tensions and expanded diplomatic space. That said, the ongoing standoff between Iran and the US over Iran’s nuclear ambitions, alongside unresolved trade tensions between the US and China, continues to complicate the GCC’s relationship with Washington in particular.

Regional Power Dynamics and Strategic Partnerships

Shifting alliances are driving a more economically aligned regional order

Power structures in the Middle East are evolving as GCC states move from being viewed primarily as a collection of energy-rich states to being recognised as increasingly sophisticated economies with clear and ambitious longterm development agendas. Saudi Arabia’s Vision 2030, the UAE’s economic diversification agenda and similar initiatives across the region are reshaping domestic economic models and external relationships.

Regional alliances are increasingly driven less by ideology or security alignment and more by shared economic interests and development priorities. The China-brokered rapprochement between Iran and Saudi Arabia represents a significant shift that has reduced regional tensions and expanded diplomatic space. That said, the ongoing standoff between Iran and the US over Iran’s nuclear ambitions, alongside unresolved trade tensions between the US and China, continues to complicate the GCC’s relationship with Washington in particular.

The Growing Influence of AI and Digital Transformation

Rapid adoption and investment positions the GCC as a leading hub for next-gen technology

Perhaps no development in 2025 has greater long-term implications than the accelerating adoption of artificial intelligence and digital technologies. As companies worldwide upgrade legacy systems, the GCC region has quickly positioned itself at the forefront of this transformation.

What began as an efficiency drive has evolved into something more fundamental. Established firms and new ventures alike are adopting cloud-native architecture, enabling them to skip intermediate stages of development. This technological leap-frogging may create a meaningful competitive advantage, particularly for the UAE.

The thirst for AI and its accompanying infrastructure has triggered substantial capital expenditure across the region. Massive investments in data centres, connectivity infrastructure, and AI research facilities are transforming parts of the Gulf into emerging technology hubs. The UAE and Saudi Arabia in particular are actively courting global AI companies, offering regulatory sandboxes, data access and capital incentives to encourage them to establish regional operations.

This focus aligns with the region’s broader economic transformation. AI is being embedded across logistics networks, free-trade zones, healthcare systems and smart-city initiatives. The GCC’s advantage lies not just in its access to financial resources, but in the ability to implement at scale without the legacy constraints that many developed markets face.

FTAs: Expanding Economic Partnerships

An expanding FTA network secures market access, deepens digital and services integration, and anchors long-term diversification

The UAE, both independently and within the GCC, has aggressively expanded its network of free trade agreements (FTAs) and comprehensive economic partnerships. This reflects a clear strategic calculation: in an increasingly fragmented global trading system, economies with the most diversified and deepest trade relationships will be the most resilient and best positioned to capture new opportunities.

Beyond the Israel-UAE CEPA, the UAE has concluded or advanced agreements with India, Indonesia, South Korea, and others. In May it started negotiations for a bilateral FTA with the European Union,with the goal of reducing tariffs, enhancing the movement of services and expanding digital and investment flows. The proposed agreement is expected to lay the groundwork for cooperation in digital trade and emerging technologies, including AI, Fintech, advanced digital infrastructure, space technologies, and smart logistics.

At the bloc-level, the GCC continues to pursue agreements that amplify the region’s collective economic weight. These agreements go well beyond traditional tariff reduction, encompassing services trade, investment protection, digital commerce, and regulatory cooperation.

The FTA strategy serves multiple purposes. It diversifies export markets for non-oil sectors, attracts foreign direct investment by providing preferential access to the GCC market, and embeds the region more deeply into global value chains. For a region historically defined by commodity exports, this growing network of economic partnerships is becoming a foundational pillar of longterm diversification.

Investment Opportunities and Risks

The convergence of macroeconomic, geopolitical, and technological shifts creates a complex landscape for investors. Equity indices in many regions are at or near record highs, and valuations in several sectors appear stretched. Navigating this environment requires a clear view of both the opportunities emerging from these trends and the risks across that accompany them.

Commodities: Beyond Traditional Energy

The Green transition is driving opportunity

While oil and gas remain central to the GCC investment thesis, the commodity landscape has broadened considerably. The energy transition is driving demand for new materials, from lithium and copper for batteries to silicon for solar panels, and several Gulf states are investing in processing and production capabilities for these critical inputs.

Natural gas, particularly liquefied natural gas, continues to see strong long-term demand as a transition fuel. The GCC’s low-cost production and expanding export infrastructure position it well to supply growing Asian markets. At the same time, investments in carbon capture, green hydrogen, and sustainable aviation fuels represent the region’s intent to play a key role in the energy system of the future as well as the present.

The key risks include the pace of energy transition, potential technological disruption in storage and renewable efficiency and policy shifts in major consuming nations. Investors will need to judge whether allocations are positioned for the long-term trajectory or vulnerable to near-term volatility.

Currency Considerations

Peg adjustments may be on the horizon, even if not imminent

For international investors, the dollar pegs maintained by most GCC currencies provide stability and eliminate direct exchange-rate risk in dollar terms. But these pegs also mean that real appreciation is delivered through inflation differentials rather than nominal exchange rate movements.

Although unlikely in the near term, eventual adjustments to the pegs or a shift toward more flexible exchange-rate regimes remain a tail risk — or, depending on positioning, a potential opportunity. The broader de-dollarisation debate, while not an immediate threat to these pegs, could eventually create pressures for reconsideration, particularly if trade patterns shift dramatically toward non-dollar economies. For regional investors and companies, managing currency risk on operations and investments outside the dollar zone will become increasingly important as trade with Asian markets continues to grow.

Cryptocurrency: down but not out

Regulatory evolution and a young , tech-forward population will continue to support crypto adoption

Cryptocurrencies, although well off their early October highs, remain a meaningful component of many investor portfolios. Cryptocurrencies have still not recovered from the 10 October meltdown when President Trump’s threats of new tariffs on China wiped out more than $1 trillion in market value across all tokens as $19 billion of leveraged positions were unwound.

Valuations have also been affected by uncertainty around the true state of the US economy and the monetary-policy outlook following the US government shutdown. Clarity should improve with the release of new economic data later in November. Despite concerns around crypto’s correlation with equities, digital assets are being mainstreamed into the global financial architecture. More than 150 cryptocurrency ETFs await approval from the US Securities and Exchange Commission, signalling rising institutional interest.

Support for cryptocurrencies may also come from their use as policy instruments in international trade and payments, as highlighted by the Carnegie Endowment for International Peace. In some contexts they may also offer countries a way to recalibrate geopolitical alliances.

Within the GCC, the UAE is taking a lead in regulatory innovation through entities such as the Virtual Asset Regulatory Authority as well as the establishment of two financial free zones. Its comprehensive framework for payment-token services and the establishment of a digital sandbox reflect a proactive approach to developing the digital-asset ecosystem. Beyond Bitcoin and Ethereum, stablecoins have emerged as the main on-chain transaction Strong grassroots adoption of crypto trading among younger people in the region, particularly in Saudi Arabia and the UAE, suggests that cryptocurrency allocations within portfolios will continue to grow.

Equity sectors: where growth capital is flowing in the GCC

Technology, renewables, and consumer-facing sectors are attracting the strongest capital flows

According to State Street Investment Management, market capitalisation across the six GCC states now exceeds $600 billion, with the region’s weight in the MSCI Emerging Markets Index rising to over six percent as of October 2025, up fourfold from its share a decade ago. The opportunity set has expanded accordingly, with several themes standing out.

Technology and digital infrastructure

—

Firms that build AI infrastructure, provide cloud services, develop fintech solutions and enable digital transformation continue to attract substantial capital. The region’s push to become a technology hub is creating winners among both established players and new entrants. Goldman Sachs notes that elevated US valuations strengthen the case for diversification toward Emerging markets, where higher nominal growth and improving market structures offer a modest advantage over Developed markets. Over time, the benefits of AI adoption are expected to stretch beyond US technology leaders.

Industrial

and Logistics

—

The GCC’s emergence as a global logistics hub, combined with efforts to develop domestic manufacturing capabilities, creates opportunities in industrial real estate, logistics services, and advanced manufacturing. The primary risks in regional equity markets include execution risk on ambitious development projects, concentration risk stemming from the dominance of government-related entities and valuation pressures in sectors where investor enthusiasm may have outpaced fundamentals. Additionally, the relatively small free float in many companies can pose liquidity challenges for larger investors.

Renewable

infrastructure

—

Schroders highlights renewables and energy-infrastructure assets as they offer strong inflation linkage, secure income characteristics and portfolio diversification through distinct risk premia such as energy prices. In general, strategies spanning energy infrastructure and real estate, both equity and debt, are backed by tangible assets that can help support more resilient returns during periods of heightened volatility.

Healthcare

and Education

—

As populations grow, private healthcare and education providers with quality offerings continue to see strong demand. These sectors benefit from both demographic tailwinds and government initiatives to expand private sector participation as well as rising consumer expectations.

Financial

Services

—

Banks and capital markets institutions are supported by robust economic growth, increasing sophistication of regional markets, and rising cross-border capital flows. The growth of Islamic finance and the region’s increasing role in global capital markets create opportunities for differentiated players.

Conclusion: A Region at an Inflection Point

From fragmentation to opportunity, understanding shifts and capturing upside

The GCC in 2025 stands at a remarkable inflection point. The convergence of diplomatic normalisation through initiatives like the Abraham Accords, aggressive AI-driven technology adoption, and an expanding web of FTAs has created an environment that would have seemed unlikely just a few years ago. Set against a global backdrop of monetary policy uncertainty, trade tensions, and currency volatility, the GCC’s relative stability, strategic positioning and proactive policies provide meaningful advantages.

For investors, policymakers, and businesses, the imperative is clear. Understand these developments as components of a larger transformation rather than in isolation as discrete trends. Opportunities are emerging across the energy transition, digital transformation and an increasingly interconnected regional economy. Realising them will require sophisticated and disciplined analysis, balancing the scale of the unprecedented opportunities with the very real risks that inevitably accompany periods of rapid change.

DISCLAIMER: This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.