From the Abraham Accords to AI to FTAs: how to trade the new Middle East

Renée Friedman, PhD

Global Head of Research

EXANTE

From the Abraham Accords to AI to FTAs: how to trade the new Middle East

The global economic and geopolitical landscape is shifting under the combined weight of uneven monetary policy normalisation, ongoing tariffs and tariff effects, an unprecedented adoption of new technologies, and a new phase of strategic realignment in the Middle East.

For investors and policymakers across the GCC, the task is to understand how these forces interact. Those who map the connections early will be best positioned to capture new avenues for trade, diversify exposure, and manage the next cycle of regional and global risk.

Renée Friedman, PhD

Global Head of Research

EXANTE

Global macro economic developments 2025

Monetary Policy: Divergence and Challenges

Sticky inflation, tariff risks and rising debt loads limit how far and how fast central banks can cut

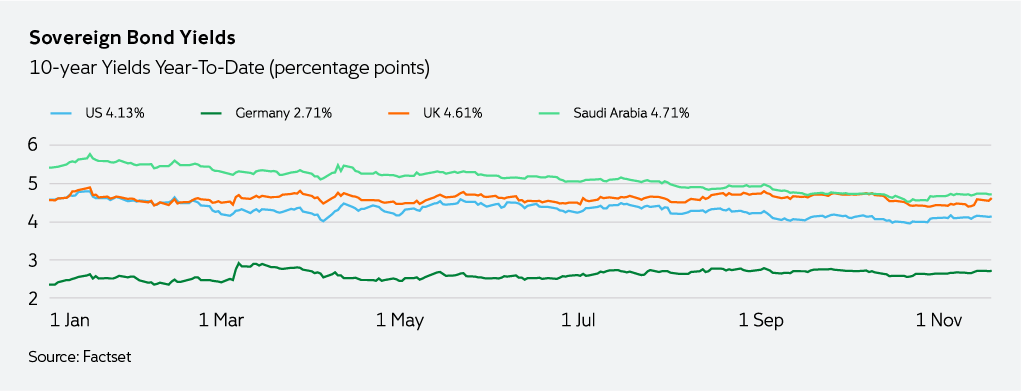

Across major economies, and with the notable exception of Japan, global monetary policies largely continued to loosen throughout 2025. The Federal Reserve held rates steady for much of the year, resuming cuts only in September and October in 25 bps increments. The European Central Bank and other G7 central banks have taken similarly cautious paths, easing in response to cooling inflation and softening growth. This overarching challenge is familiar. A delicate balancing act between supporting labour markets while still anchoring inflation expectations.

Bond market performance has been largely positive due to this normalisation. But inflation remains stickier than expected across many economies and US tariff uncertainty imposes additional upward pressure for 2026. At the same time, there are concerns over growing debt levels. Six of the G7 countries are expected to see debt-to-GDP exceed 100 percent in 2025, sharpening concerns around fiscal flexibility.

This dynamic is particularly acute in the US and UK, where higher borrowing costs and narrowing fiscal headroom are negatively impacting market sentiment. As questions around debt sustainability rise and sovereign debt continues to flood the market, investors may demand higher yields, tightening financial conditions and adding pressure to public finances. The interaction matters. Higher debt levels and rising debt loads can amplify market volatility, especially if the cost of capital increases. In that event, companies may struggle to fulfill their capex goals on AI, thereby potentially busting the bubble that has driven equity markets throughout this year.

The growth of fiscal dominance

Elevated debt heightens political pressure on central banks and complicates the path of monetary policy

Rising debt burdens have brought the spectre of fiscal dominance back into focus. In such an environment, central banks face growing political pressure to keep rates low or to accommodate government spending through money creation. It can reignite inflation, undermine central bank independence, and erode confidence in state institutions.

In the United States, these concerns have sharpened. Investor unease stepped up several notches following President Trump’s attempts earlier this year to dismiss Federal Reserve Governor Lisa Cook and his public criticism of Chair Jerome Powell for not cutting rates more quickly. Attention is increasingly being focussed on the President’s choice for Powell’s successor, with his term as Chair set to end in May 2026. With inflation now near 3 percent in the US, if President Trump continues to push for lower headline rates, it could push real interest rates into negative territory. This, in turn, would encourage borrowing and investment and certainly risk higher inflation.

The tension between political expediency and monetary prudence is likely to intensify as debt levels remain elevated and the 2026 US midterms approach. These dynamics, however, should have limited impact on the GCC. According to the International Monetary Fund (IMF), GCC economies are expected to sustain solid growth with low inflation and strong current account and external financial positions over the next five years. The region’s substantial sovereign wealth funds provide an additional buffer against fiscal stress, though the World Bank notes that downward pressure on oil prices will weigh on government revenues, increasing fiscal strains in Kuwait, Oman and the UAE.

AI lifts markets, but risks accumulate

Enthusiasm for all things AI lifted global equities to new highs, but the rally is vulnerable

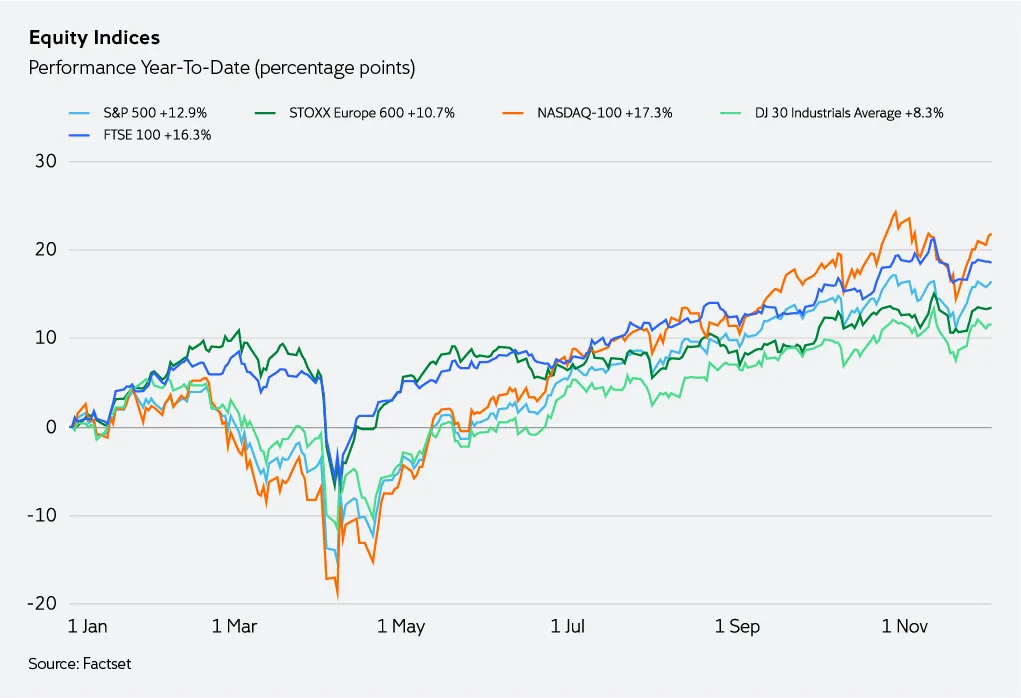

Global equity markets have recovered steadily since the April “Liberation Day” sell-off. Expectations of Fed policy easing and continued momentum in the AI revolution have pushed indices to fresh highs. Yet the headline rally masks a more nuanced backdrop. Markets are late in the cycle and the bull market euphoria remains tightly linked to the Fed’s next moves. Without further rate cuts, the current momentum could prove fragile.

At the same time, additional easing — especially if paired with expanded fiscal stimulus — may accelerate the cycle rather than extend it. As Andrew Slimmon at MorganStanley notes, the more liquidity, the higher the speculative stocks rise. And the faster the bubble inflates, the faster the market moves through the “euphoria stage”, increasing the risk of a sharper reversal.

AI lifts markets, but risks accumulate

Enthusiasm for all things AI lifted global equities to new highs, but the rally is vulnerable

Global equity markets have recovered steadily since the April “Liberation Day” sell-off. Expectations of Fed policy easing and continued momentum in the AI revolution have pushed indices to fresh highs. Yet the headline rally masks a more nuanced backdrop. Markets are late in the cycle and the bull market euphoria remains tightly linked to the Fed’s next moves. Without further rate cuts, the current momentum could prove fragile.

At the same time, additional easing — especially if paired with expanded fiscal stimulus — may accelerate the cycle rather than extend it. As Andrew Slimmon at MorganStanley notes, the more liquidity, the higher the speculative stocks rise. And the faster the bubble inflates, the faster the market moves through the “euphoria stage”, increasing the risk of a sharper reversal.

Unlock the full report — just tell us a bit about yourself